Office of the Commission

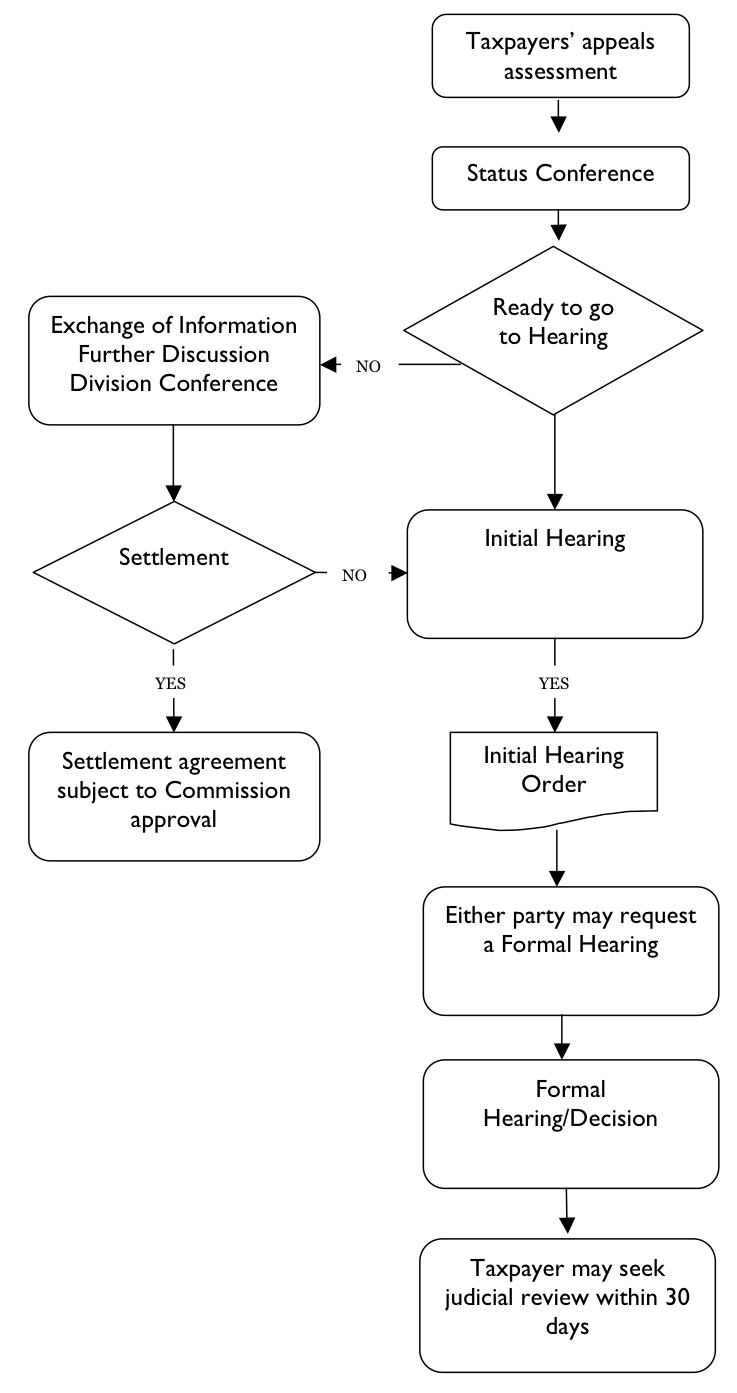

Appeals of Audit Assessments

The Commission’s Income Tax and Education Division and Business Taxes and Discovery Division issue notices of deficiencies of individual income tax, corporate franchise tax, sales tax, fuel tax and other tax types. For detailed information about audits please see audits.

A notice of deficiency may be appealed through the Commission’s appeals process pursuant to Utah Code Sec. 59-1-501. The taxpayer must file the appeal within 30 days of the date of the notice of deficiency, or the the deficiency becomes the final assessment.

In our experience, most of the disputes arising from income tax audit assessments are resolved through interaction or negotiation between parties. Therefore, most of these appeals are routinely scheduled for a telephone status conference with an Administrative Law Judge, who screens the case, defines the issues and allows the parties additional time to work toward a resolution, if appropriate. If the parties reach agreement, the Commission will issue an order approving the agreement or accepting a withdrawal of the appeal. If this process does not result in a settlement, the matter proceeds to a hearing.

Appeals Process

- Petition for appeal must be filed within 30 days of the notice of deficiency.

- The matter is generally scheduled for a status conference before an Administrative Law Judge.

- The parties are allowed additional time to exchange information, pursue resolution of associated dispute with IRS or otherwise work toward an agreement to resolve some or all of the pending issues.

- As new information becomes available, the audit findings may be amended or reversed. The parties may enter a settlement agreement that disposes of the appeal.

- If the parties cannot settle the dispute between them, or if the issue is a purely legal matter that requires a decision by the Commission, the matter is scheduled for a hearing.

- The appeal is set for an Initial Hearing, unless waived by the parties. The Commission’s Initial Hearing decision is subject to a request for a Formal Hearing.

- If a Formal Hearing has been held, once the Formal Hearing decision has been issued by the Commission, the taxpayer may seek judicial review of the Commission’s Formal Hearing decision within 30 days.