Tax Commission

Grocery Food Sales & Use Tax

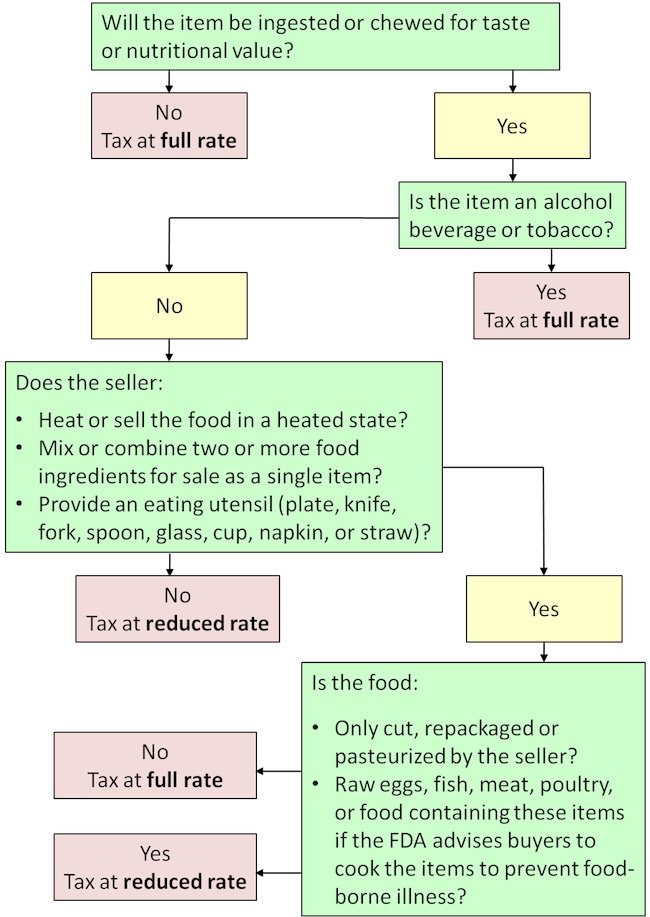

Grocery Food Sales Tax Flowchart

The statewide grocery food sales tax rate is 3 percent. The following flow chart will help you decide what should be taxed at this lower rate.

Product List: Food versus Non-Food Matrix

| Product Description | Food | Non Food or Prepared Food | Comments |

|---|---|---|---|

| Breath Mints | x | Nutritional or supplemental fact box on label means item is food. Drug fact box on label means item is not food. | |

| Chicken meal deal | x | Example: 8 pieces/salad/rolls | |

| Deli meats by weight | x | Cut and repackaged by seller | |

| Deli salad by size or weight | x | If utensils* are not available in the area | |

| Deli salsa by size or weight | x | Made in the store | |

| Deli sandwich by weight | x | If made by seller | |

| Donuts without utensils* | x | If utensils* are not available in the area | |

| Hot French bread | x | ||

| Ice, block | x | Ice sold in blocks or dry ice is used for cooling and is not food | |

| Ice, crushed | x | Ice sold by a food retailer in cubes or crushed can be ingested for taste | |

| Ice, dry | x | Ice sold in blocks or dry ice is used for cooling and is not food | |

| Meat/cheese platter, set price | x | ||

| Meat/cheese platter, sold by weight | x | ||

| Mixed fruit tray, price per tray | x | ||

| Mixed fruit tray, sold by weight | x | ||

| Nutritional supplements | x | Nutritional or supplemental fact box on label means item is food. Drug fact box on label means item is not food. | |

| Pam (non-stick spray for pans) | x | ||

| Pet food | x | ||

| Produce plastic bags or mesh bags with twist ties | x | Retailer buys tax exempt and builds into price of product | |

| Pumpkin seeds | x | If packaged for eating | |

| Rock salt | x | Rock salt is less pure and is commonly used for ice cream making | |

| Salad bar sold by weight | x | If utensils* are not available in the area | |

| Self-serve fountain drinks | x | 16, 32, 48 oz. cups | |

| Shiskabobs made in store | x | Raw meat | |

| Store-dyed Easter eggs | x | ||

| Sunflower seeds | x | If packaged for eating | |

| Toothpaste | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Vaporizer/humidifier | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Vegetable garden seeds | x | ||

| Vitamins | x | Nutritional or supplemental fact box on label means item is food. Drug fact box on label means item is not food. | |

| Vitamins for hair loss | x | Nutritional or supplemental fact box on label means item is food. Drug fact box on label means item is not food. | |

| Water, bottled (including flavored) | x | ||

| Water, distilled | x |

| Medications (over the counter) | Food | Non Food or Prepared Food | Comments |

|---|---|---|---|

| Antacids | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Anti-diarrhea | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Anti-gas | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Anti-smoking patches | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Breath sprays | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Breath strips | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Cough drops | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Ear drops | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Epson salts | x | ||

| Eye drops | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Laxatives | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Medication for hair loss | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Motion sickness | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Nasal sprays | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Oral antismoking | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Pain/headache | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Sleep aid | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. | |

| Throat sprays | x | Drug fact box on label means item is not food. Nutritional or supplemental fact box on label means item is food. |

Examples

Example #1:

You sell milk and bread to a customer. These items are grocery food so you collect tax at the grocery food rate (3 percent) at checkout.

Example #2:

You sell milk, bread and clothing in one transaction. The milk and bread are grocery food, but the clothing is not. You collect tax at the grocery food rate (3 percent) on the grocery food and the combined sales tax rate at your location for the clothing.

See current rates.

Example #3:

You prepare and sell a fruit basket in a wicker basket as one item. The fruit is grocery food, but the wicker basket is not.

Sales of two or more grocery food and non-food items combined products sold for one price are bundled transactions.

You collect the full combined sales tax rate at your location on the whole fruit basket.

See current rates.

Example #4:

You sell a combo meal that includes a sandwich, chips and drink.

The combo meal is prepared food sold for one price as a bundled transaction. You collect the full combined sales tax rate at your location (plus the restaurant tax, if applicable).

See current rates.

Industry-Specific Examples

Bakery Items

Bakery items include the following if you sell them without providing eating utensils:

- Bagels

- Bars

- Biscuits

- Bread

- Buns

- Cakes

- Cookies

- Croissants

- Danishes

- Donuts

- Muffins

- Pastries

- Pies

- Rolls

- Tarts

- Tortes

- Tortillas

Examples:

- You own a bakery and sell donuts. You do not provide utensils so the food is taxed at the reduced rate.

- You own a restaurant and sell a customer some of your rolls. These are grocery food items. Because the sale occurs in a restaurant, tourism tax applies on the transaction.

- If you sell the rolls with utensils, the rolls are prepared food taxed at the full combined rate plus tourism (restaurant) tax.

- If you sell the rolls without utensils, the rolls are grocery food taxed at the lower rate plus tourism (restaurant) tax.

Deli Inside a Store

Prepared food is:

- Food sold in a heated state or heated by a seller.

- Two or more food ingredients mixed or combined by a seller for a single sale.

- Food sold with an eating utensil provided by the seller (plate, knife, fork, spoon, glass, cup, napkin, straw, etc.).

Prepared food is not:

- food that a seller only cuts, repackages, or pasteurizes

- raw eggs, raw fish, raw meat, raw poultry, or a food containing these items if the Food and Drug Administration (FDA) advises buyers to cook the items to prevent food borne illness.

Examples:

You own a store with a self-serve salad bar and deli. You provide eating utensils for both the salad bar and deli. Your customer:

- Makes a salad at the salad bar. You weigh and price it at the cash register. This is prepared food taxed at the full rate. If you do not provide utensils, the salad is grocery food taxed at the lower rate (because it is unheated and sold by weight).

- Buys fried chicken and a pound of sliced cheese at your deli. The fried chicken is prepared food taxed at the full rate. The sliced cheese is grocery food taxed at the lower rate because it was only cut and repackaged.

- Buys a pound of potato salad you made in your deli. The potato salad is prepared food taxed at the full rate. If you do not provide utensils, the potato salad is grocery food taxed at the lower rate (because it is unheated and sold by weight as a single item).

Vending Machine Sales

Answer the following four questions to determine the sales tax rate for a vended item:

- What is the item? Vended items that cannot be ingested (nail clippers, combs, toys, etc.) are taxed at full rate.

- Is the item heated by the seller? In part, prepared food is “sold in a heated state or heated by a seller.” If heated, the vended item is prepared food and taxed at the full rate.

- Does the seller make utensils available to the buyer? A purchase is prepared food taxed at the full rate if you provide tables & chairs, condiments, a microwave, or utensils (plate, knife, fork, spoon, glass, cup, napkin, or straw) in the area near the vending machines.

- Does the item have two or more food ingredients mixed by the seller? In part, prepared food is sold “with two or more food ingredients mixed or combined by the seller.”

Examples:

- Pack of gum from a vending machine – grocery food taxed at lower rate

- Bag of chips or can of soda – grocery food taxed at lower rate

- Pre-mixed cup of hot chocolate – prepared food taxed at full rate

- Slice of pizza you heat – prepared food (preheated) taxed at full rate

- Slice of pizza your customer heats – prepared food (two or more ingredients mixed by the seller) taxed at full rate

- Sandwich – prepared food (two or more ingredients mixed by the seller) taxed at full rate

- Vitamins and Food Supplements

- Vitamins and food supplements are grocery food taxed at the lower rate.

Sales Tax: Full Rate and Reduced Rate Industry Chart

Effective January 1, 2007

| Seller | Item | Sales Tax Rate | Restaurant Tax | Notes |

|---|---|---|---|---|

| Grocery Store | Grocery food | Reduced | No | |

| Grocery Store | Non-food items | Full | No | |

| Grocery Store | Salads prepared by seller | Full | No | 1 |

| Grocery Store | Salad bar with utensils | Full | No | 1 |

| Grocery Store | Salad bar, no utensils | Reduced | No | 3 |

| Grocery Store | Deli items (meat, salad) with utensils | Full | No | 1 |

| Grocery Store | Deli items (meat, salad) no utensils | Reduced | No | 3 |

| Grocery Store | Bakery items with utensils | Full | No | 1 |

| Grocery Store | Bakery items no utensils | Reduced | No | 3 |

| Grocery Store | Rotisserie items | Full | No | 1 |

| Grocery Store | Restaurant inside grocery store | Full | Yes | 1,2 |

| Grocery Store | Food court inside store | Full | Yes | 1,2 |

| Restaurant, stand alone | Prepared food | Full | Yes | 1,2 |

| Restaurant, stand alone | Grocery food | Reduced | Yes | 3 |

| Restaurant, stand alone | Candy bars, etc. | Reduced | Yes | 3 |

| Edible Items Purchased in Restaurants | Purchase a pie, muffins, rolls, etc. from restaurant no utensils | Reduced | Yes | 3 |

| Edible Items Purchased in Restaurants | Purchase a pie, muffins, rolls, etc. from restaurant with utensils | Full | Yes | 1 |

| Bagel/Donut Shop | Bagels, donuts with napkin | Full | Yes | 2 |

| Bagel/Donut Shop | Prepackaged container of cream cheese, milk or juice with utensils | Full | Yes | 1 |

| Bagel/Donut Shop | Prepackaged container of cream cheese, milk or juice no utensils | Reduced | Yes | 3 |

| Convenience Store | Soft drinks in cooler | Reduced | No | 3 |

| Convenience Store | Soft drinks from fountain | Full | No | 1,2 |

| Convenience Store | In-store restaurant (sandwich shop, etc.) | Full | Yes | 1,2 |

| Convenience Store | Grocery food | Reduced | No | 3 |

| Convenience Store | Hot dogs, burritos, etc. | Full | No | 1 |

| Pizza | Delivered to customer’s location | Full | Yes | 1 |

| Pizza | Consumed at pizza restaurant | Full | Yes | 1,2 |

| Pizza | “Take & bake” cooked at home | Full | No | 1,2 |

| Dinner Theater | All | Full | Yes | 1,2 |

| Movie Theater | Fountain drinks | Full | No | 1,2 |

| Movie Theater | Candy bars | Reduced | No | |

| Movie Theater | Popcorn, etc. | Full | No | 1,2 |

| Bakery, traditional | Grocery food | Reduced | No | 3 |

| Medications | Non-prescription over-the-counter items such as aspirin, cough drops, etc. that are ingested or chewed. Please see Product Matrix. | Full | No | |

| Medications | Prescription items that qualify as a drug | Tax exempt | No |

Additional Information

See Publication 25, Sales and Use Tax General Information.

You may also call the Tax Commission at (801) 297-7705 or toll free at 1-800-662-4335 ext. 7705 or email to [email protected].

Definitions

Bundled Transactions

The retail sale of two or more separate products sold for one combined price.

If any part of the bundled transaction is taxable, the entire transaction is taxed (unless the seller keeps separate records of the tax-exempt part of the transaction).

Drug

A compound, substance, or preparation used to diagnose, cure, mitigate, treat, or prevent disease or to affect the structure or function of the human body.

Grocery Food

Substances sold for ingestion or chewing by humans for taste or nutrition. Grocery food does not include alcoholic beverages, tobacco or prepared food.

Grocery food includes items sold without eating utensils by a food maker (other than a bakery and tortilla maker), items sold singly and unheated by weight or volume, and bakery items (bagel, bar, biscuit, bread, bun, cake, cookie, croissant, danish, donut, muffin, pastry, pie, roll, tart, torte or tortilla). A container or packaging used to transport food is not considered an eating utensil.

Prepared Food

- Food sold in a heated state or heated by a seller.

- Two or more food ingredients mixed or combined by the seller for a single sale.

- Food sold with an eating utensil provided by the seller (plate, knife, fork, spoon, glass, cup, napkin, or straw, etc.).

Prepared food does not include:

- food that a seller only cuts, repackages, or pasteurizes

- raw eggs, raw fish, raw meat, raw poultry, or a food containing these items if the Food and Drug Administration (FDA) advises buyers to cook the items to prevent food borne illness.

Purchase Price and Sales Price

The total value for which tangible personal property, products transferred electronically or services are sold, leased or rented. Purchase price and sales price include:

- the seller’s cost of the tangible personal property, products transferred electronically or services;

- the seller’s expenses, including:

- the cost of materials,

- labor cost,

- service cost,

- interest,

- a loss,

- the cost of transportation to the seller, and

- tax (including federal excise tax) imposed on the seller; and

- charges by the seller for any service necessary to complete the sale.

Purchase price and sales price do not include:

- delivery charges;

- installation charges;

- cash discounts or discount terms offered to buyers;

- coupons that are not reimbursed by a third party; or

- the following, if separately stated on an invoice, bill of sale or similar document given to the buyer:

- the amount of a trade-in;

- interest, financing and carrying charges for credit extended on the sale of tangible personal property, products transferred electronically or services; and

- a tax or fee legally imposed directly on the buyer.

Restaurant

A retail establishment whose business is the sale of food and beverages for immediate consumption. The definition of “restaurant” does not include theaters, but does include dinner theaters. See Utah Code Ann. §59-12-602.

Exception: In counties that impose the tourism tax, it does not apply to food sales from deli areas, pizza take-out counters or salad bars within a grocery store or convenience store whose primary business is the sale of fuel or food not prepared for immediate consumption. These sales are exempt from the tourism tax even if the store has seats or stools for customers. However, if a grocery or convenience store has a full-service restaurant, the tourism tax is due on sales in that restaurant.