Office of the Commission

General Information

Property tax is based on a property's fair market value as of January 1 of each tax year. For locally assessed real property, which is property that is assessed by a County Assessor, the County Assessor must determine the fair market value for that property each year as of January 1. Counties use computer-assisted mass appraisal systems to determine the market value for each parcel of real property each year and issue the initial valuation notice, which must be mailed to the property owner no later than July 22 of each tax year.

County Board of Equalization (BOE)

Property owners may dispute their property's value by filing an appeal with the County Board of Equalization in the county where the property is located. The deadline to file an appeal is generally September 15 for each tax year. The property owner is required to provide some evidence to support the lower value. Once the property owner has filed a completed appeal and achieved standing before the County BOE, the County BOE will issue a written decision. Late filed appeals are accepted only under very limited criteria specified in statute and administrative rule. Once the County BOE issues its decision, the County BOE’s decision is appealable to the Utah State Tax Commission. However, there is a statutory deadline to file the appeal, which is thirty days from the date on the County’s decision.

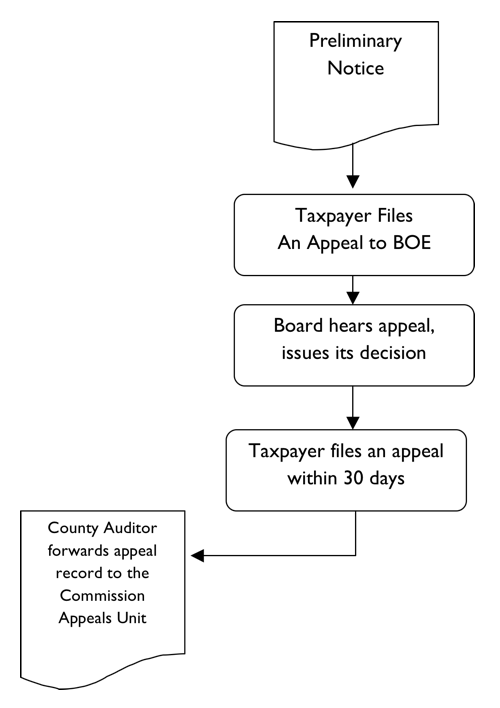

County Board of Equalization Process

- Preliminary valuation notice issued no later than July 22.

- Property owner may appeal the property valuation to the County Board of Equalization by September 15.

- The County Board of Equalization hears the appeal and then issues a written decision.

- The County BOE decision may be appealed to the Utah State Tax Commission within thirty days from the decision date. Appeals from Board of Equalization decisions proceed through the Tax Commission Appeals Unit process.

Commission Appeal Process for Locally Assessed Property

To file an appeal to the Commission, for locally assessed property the party must file a TC-194 with the County Auditor within 30 days of the date on the County Board of Equalization decision. The County Auditor attaches the hearing record and forwards the appeal record to the Tax Commission’s Appeals Unit.

The Tax Commission Appeals Unit receives the record from the County Auditor and the appeal is entered into the Appeals Unit’s case management database. The appeal will then be scheduled for its first step in the Tax Commission’s administrative hearing process, which is either a Mediation Conference or an Initial Hearing. A Notice of the event will be sent to parties by mail or e-mail. The Mediation or Initial Hearing will be held before an Administrative Law Judge or Tax Commissioner. Events are held by video conference, unless either party requests an in-person hearing. In-person hearings are generally held in the Salt Lake Offices of the Utah State Tax Commission.

If the matter is scheduled for a Mediation Conference, either party may opt out of the mediation and request an Initial Hearing instead. If the case is set for an Initial Hearing and you would like to try mediation, you may present that idea to the opposing party. If all parties agree to mediate the case, the Tax Commission will support that decision.

If the parties are not able to reach an agreement in the mediation, the appeal will be scheduled for the second step of the process, a Formal Hearing. If instead an Initial Hearing had been held in the appeal, and a party disagrees with the Initial Hearing Order, the party may request a Formal Hearing. If both parties agree, the parties may waive the first step in the administrative appeal process and have the appeal scheduled directly for a Formal Hearing.

Evidence

When the real property appeal is scheduled for either an Initial Hearing or a Formal Hearing, the parties should be presenting evidence of the market value of the property as of the January 1 lien date. Or evidence on equalization from assessments made for the tax year at issue in the appeal.

The evidence should be sent to the Commission and the County ten business days prior to the hearing. If you fail to send your evidence documents to the County ten business days prior to the hearing, it is possible that your evidence will not be considered in the decision.

Submittal of Documents

The Tax Commission Appeals Unit will accept all written submissions and forms by facsimile, e-mail, or mail.

E-mail: [email protected]

Mailing Address:

Utah State Tax Commission Appeals Unit

1950 West 210 North

Salt Lake City, Utah 84134

Fax: 801-297-3919

Settlement Discussions

Parties are encouraged to continue settlement discussions. Neither the filing of an appeal nor any proceedings scheduled during the appeal process precludes further discussion or negotiation between the parties. The Tax Commission fully supports and encourages continued interaction between the parties to attempt to reach an agreement on the outstanding issues. If the parties reach an agreement prior to any proceeding, the Commission will generally issue an order approving the stipulated value.